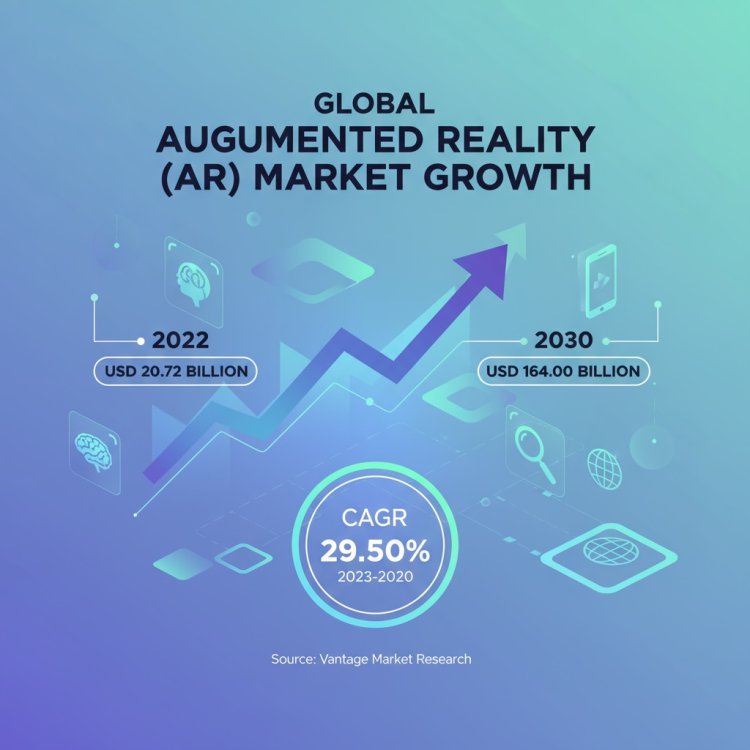

Global Augmented Reality (AR) Market Size, Share & Forecast 2023–2030 | CAGR of 29.50%

Explore the Global Augmented Reality (AR) Market valued at USD 20.72 Billion in 2022, projected to reach USD 164.00 Billion by 2030, growing at a CAGR of 29.50%. Get insights on trends, growth drivers, and forecasts.

Global Augmented Reality (AR) Market to Reach USD 164.00 Billion by 2030, Driven by 29.5% CAGR

The global Augmented Reality (AR) market continues a robust expansion trajectory, driven by increasing adoption across technology, enterprise, healthcare, and consumer sectors. Based on the most recent Vantage Market Research data, the AR segment—distinct from VR or extended reality (XR)—is poised to deliver significant long-term growth. Key players are innovating across hardware, software, and applications, backed by substantial investment and rising market penetration.

Our comprehensive Augmented Reality (AR) Market report is ready with the latest trends, growth opportunities, and strategic analysis. View Sample Report PDF.

Key Takeaways

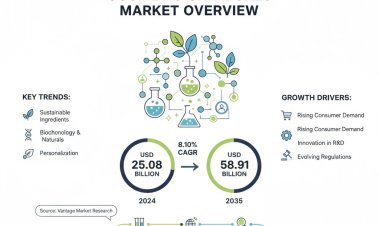

- According to Vantage Market Research, the global Augmented Reality (AR) market saw notable revenue in 2024 and is forecasted to exponentially expand through 2035.

- Compound annual growth rates (CAGR), segmentation insights (technology, offering, device type, application, region), and industry drivers are clearly defined for strategic analysis.

- The North American region currently leads in market size, while Asia Pacific is anticipated to grow fastest.

- Recent developments in AR hardware (e.g., smart glasses launches and strategic investments) underscore vibrant momentum across the ecosystem.

Premium Insights

Revenue 2024: As per Vantage, the global AR market—encompassing technology, offering, device type, and application—reported a 2022 baseline of USD 20.72 Billion with projection to USD 164.00 Billion by 2030 at a 29.5% CAGR. Although Vantage does not specifically report 2024 revenue for the generic AR market, this remains the most relevant Vantage figure available.

The AR market is characterized by strong adoption across enterprise, healthcare, retail, and automotive sectors, encouraged by technological convergence (5G, mobile sensors), and increasing investment in immersive experiences. Growth is particularly driven by markerless and anchor-based technologies, rising use of HUDs and HMDs for industrial and automotive applications, and an expanding ecosystem of software solutions enhancing interoperability and ease of deployment.

Market Size & Forecast

- 2022 Estimated Revenue: USD 20.72 Billion

- 2030 Forecast: USD 164.00 Billion at a CAGR of 29.5% (2023–2030) .

The AR market is moderately fragmented, with technology giants (e.g., Apple, Google, Meta) dominating in hardware and platform offerings, while numerous niche players and service providers specialize in specific verticals such as enterprise training, healthcare, and retail. Regulatory, privacy, and integration challenges influence competitive dynamics and adoption speed.

For Augmented Reality (AR) Market Research Report and updates detailed: View Full Report Now!

Technology Insights

The AR market by technology includes marker-based, markerless, and anchor-based AR. Marker-based AR is widely used in advertising and gaming, requiring visual triggers for experiences. Markerless AR, powered by AI and advanced sensors, is increasingly popular for retail, navigation, and healthcare as it eliminates reliance on physical markers. Anchor-based AR is gaining traction in industrial and automotive sectors, enabling spatial overlays tied to real-world coordinates. Together, these technologies diversify applications and fuel rapid adoption across industries.

Offerings Insights

The AR market by offerings is split into hardware and software. Hardware—such as HUDs, HMDs, and AR smart glasses—forms the backbone for immersive experiences, particularly in automotive, enterprise, and healthcare. Meanwhile, software solutions drive scalability by offering AR development kits, platforms, and content creation tools, enabling seamless integration across devices and verticals. With advances in markerless and AI-driven AR, software is becoming the growth catalyst, while hardware innovation ensures performance improvements and wider consumer acceptance.

Device Type Insights

Device types in the AR market include Head-Up Displays (HUDs) and Head-Mounted Displays (HMDs). HUDs are widely deployed in automotive and aviation to project critical information directly into the user’s line of sight, improving safety and convenience. HMDs, such as AR glasses and enterprise headsets, dominate in industrial, healthcare, and training environments by delivering immersive, hands-free experiences. As hardware becomes lighter and more affordable, both HUDs and HMDs are increasingly penetrating consumer, enterprise, and defense markets.

Application Insights

Applications of AR span automotive, retail, healthcare, industrial/manufacturing, and education. In automotive, AR enhances driver navigation and safety via HUDs. Retail benefits from AR-powered virtual try-ons and immersive shopping experiences. Healthcare leverages AR for surgical training, diagnostics, and patient care. Industrial applications focus on AR-guided maintenance, assembly, and remote collaboration. Education uses AR for interactive, experiential learning. Each application reflects the adaptability of AR technologies, driving cross-sector adoption and transforming traditional workflows with real-time, contextual experiences.

Regional Insights

North America

North America leads AR adoption, supported by strong digital infrastructure, early consumer acceptance, and industry innovation from Silicon Valley to Boston. AR technologies are integrated into automotive dashboards, enterprise training programs, healthcare simulations, and retail experiences. The presence of key developers (Apple’s ARKit, Google ARCore, Meta’s Reality Labs) drives platform availability and developer engagement. The region’s regulatory clarity and investment landscape further propel market maturity and commercialization across consumer and industrial sectors.

Europe

Europe’s AR growth is driven by manufacturing adoption (Industry 4.0 use cases in Germany, automotive in UK and France) and healthcare applications across Scandinavia and Western European nations. Retailers use AR for immersive shopping, and cultural sectors (museums, tourism) leverage it for engagement. EU investments in digital transformation and spatial computing regulations enhance adoption. While regulatory standards are evolving, the region demonstrates strong cross-sector experimentation and application of markerless and anchor-based AR in both enterprise and consumer contexts.

Asia Pacific

Asia Pacific is the fastest-growing region, driven by robust smartphone penetration, government digital initiatives (China, India, South Korea), and manufacturing hubs deploying AR in training and production. Retailers and e-commerce players incorporate AR for virtual fitting and visualization, especially in urban markets. Markerless AR is prevalent via mobile platforms. Rapid 5G rollout, affordable hardware, and tech adoption in education and healthcare further accelerate growth. Countries like China and India are emerging as both large consumer bases and innovation centers for AR applications.

Latin America

Latin America shows rising AR adoption driven by urban retail innovation and education. Large markets like Brazil and Mexico integrate AR for virtual try-on in fashion and ecommerce, as well as immersive educational tools in schools. Mobile-first strategies harness markerless AR via smartphones. Infrastructure variability and cost sensitivity slow uptake, but pilot projects in healthcare, tourism, and retail demonstrate growing interest. Regional players increasingly adopt low-cost AR solutions, while cross-border collaborations expand access and awareness.

Middle East & Africa

Middle East & Africa display nascent yet promising AR adoption, mainly in tourism (immersive guides in UAE, Saudi Arabia), retail marketing, and educational pilots. Smart city initiatives and digital transformation in Gulf Cooperation Council (GCC) countries drive AR integration for public services and events. Adoption hurdles include infrastructure gaps and investment limitations. However, markerless mobile AR facilitates reach via smartphones, and partnerships with global AR providers support regional scalability. Growth potential lies in cultural tourism, real estate visualization, and educational innovation.

Top Key AR Companies

- GOOGLE INC.

- PTC INC.

- SEIKO EPSON

- MICROSOFT

- LENOVO

- SAMSUNG ELECTRONICS

- Apple Inc.

- WIKITUDE GMBH

- MAXST CO. LTD.

- QUALCOMM

- TOSHIBA CORPORATION

- UPSKILL

- BLIPPAR

- VISTEON CORPORATION

- GLOBE TECHNOLOGIES

- OPTINVENT

- MAGIC LEAP INC.

- MARXENT LABS LLC

These companies significantly shape technology, platform adoption, and end-user experiences across mobile, wearable, and enterprise AR ecosystems.

Recent Developments (2024–2025)

- Snap Inc. announced plans to commercially launch its next-generation AR smart glasses, called Specs, in 2026, featuring a thinner, lighter design and AI-powered spatial experiences backed by partnerships with OpenAI, Google, and Niantic Spatial.

- Meta Platforms acquired a nearly 3 % stake (~$3.5 billion) in EssilorLuxottica, its Ray-Ban smart glasses partner, reinforcing its AR eyewear ambitions. With over two million Ray-Ban Meta smart glasses sold since 2023 and anticipated annual growth over 60% through 2029, Meta continues to stake its future on wearable AR as a potential smartphone successor.

Market Scope

This press release synthesizes insights from Vantage Market Research on the global Augmented Reality (AR) market, providing a comprehensive analysis of revenue trends, growth forecasts, and strategic opportunities. The scope covers detailed segmentation by technology (marker-based, markerless, anchor-based AR), offerings (hardware, software), device type (HUDs, HMDs), application (automotive, retail, healthcare, industrial, education), and region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa). It highlights 2024 revenue estimates, 2030 forecast, and CAGR (2025–2030), along with competitive landscape insights, key company strategies, recent developments, and emerging growth opportunities shaping the AR industry.

Market Dynamics

Driver

Technological advancements—5G networks, improved sensors, and AI—drive AR adoption by enabling seamless, markerless experiences across mobile and wearable devices. Industries such as automotive, healthcare, retail, and manufacturing leverage AR to improve safety, efficiency, customer engagement, and training outcomes. User familiarity with digital interfaces, enterprise digital transformation, and increasing R&D investments further accelerate AR deployment. These combined factors make AR a strategic growth domain across hardware, software, and application ecosystems.

Restraint

AR growth faces challenges including privacy concerns (especially for camera-enabled smart glasses), high hardware costs, and comfort/usability issues. Enterprise adoption may be slowed by integration complexity and limited developer expertise. Regulatory hurdles around data capture, surveillance, and visual distraction provision further complicate implementation, particularly in public or sensitive settings. These barriers may delay mass uptake and require mitigation strategies to ensure broader AR acceptance.

Opportunity

AR presents opportunities in immersive customer experiences (e-commerce, tourism, gaming), enterprise efficiency (remote assistance, training), and healthcare (surgical guidance, diagnostics). The rising popularity of AR glasses, integration of AI, and platform-based ecosystems (ARKit, ARCore, Lightship) open new use-case possibilities. Emerging markets with mobile penetration and digital initiatives (e.g., Asia Pacific, Latin America) offer expansion potential. Custom SDKs tailored to vertical needs also unlock scalable solutions, creating paths for sustainable monetization.

Challenges

Challenges include user discomfort with wearing AR devices, limited battery life, weight, and visual fatigue. Standardization across platforms remains lacking, hindering interoperability. Content creation can be costly and time-consuming, while legacy systems may not integrate seamlessly with AR. Public skepticism and cultural resistance, particularly outside technology hubs, can slow adoption. Overcoming these requires ergonomic design, open standards, developer education, and compelling use cases tailored to specific markets and demographics.

Global Augmented Reality Market Segmentation

- By Technology: Marker-Based AR, Markerless AR, Anchor-Based AR

- By Offering: Hardware, Software

- By Device Type: HUDs, HMDs

- By Application: Automotive, Retail, Healthcare, Industrial, Education (implied)

- By Region: North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Frequently Asked Questions

- What was the AR market size in 2022?

Vantage reports a 2022 baseline of USD 20.72 Billion.

- What is the forecast through 2030?

Vantage forecast: USD 164 Billion by 2030 at a CAGR of 29.5%.

- What segments drive the AR market?

Key segments include marker-based, markerless, anchor-based technologies; hardware vs. software offerings; HUDs/HMDs; multiple application verticals; and five major regions .

- Which region leads adoption?

North America is currently the largest AR market; Asia Pacific is fastest-growing.

- What are recent AR developments?

Snap plans to launch its AI-enabled Specs in 2026. Meta made significant investment in AR eyewear and reports strong smart glasses sales